The Capital Stack that Built the City - Part 1

Why Paris Built Apartments and London Built Row Houses: The Political Economy of Continental and Anglo Urban Form

The 1910 gap

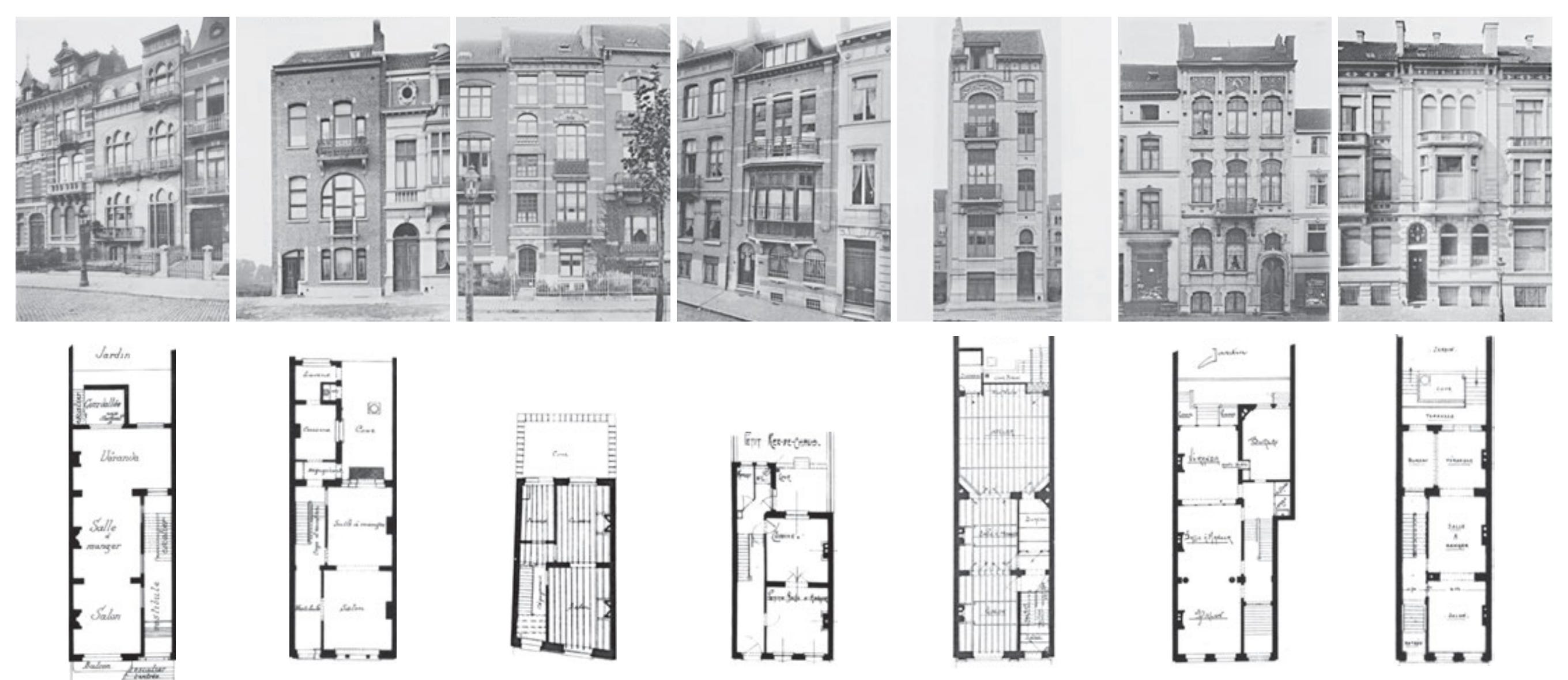

In 1700 the major Western cities looked broadly alike. Walking through London, Paris, Amsterdam, Madrid, Berlin, Rome, Naples or Brussels, you would have passed mostly low-rise, narrow-fronted buildings - what we would today call row houses or town houses, single buildings each held in some local approximation of freehold. There were exceptions. Edinburgh’s Old Town had its tall stone “lands”. A few Roman insulae survived in pieces of Naples and Rome. The grand Italian palazzi of Genoa and Venice were subdivided across their stories. But the dominant urban dwelling, from Madrid to Manchester, was a single house, ground to roof, with one front door.

By 1910, a hard line ran across the West. On one side were London, Manchester, Birmingham, Liverpool, Bristol, Brooklyn, Boston, Philadelphia, Amsterdam, Antwerp, Brussels - row-house cities, with narrow plot frontages, low-rise terraces or detached and semi-detached houses, mostly built by small jobbing builders and, where they were owned at all, held by petty proprietors.

On the other side were Paris, Berlin, Vienna, Madrid, Barcelona, Milan, Turin, Budapest, Rome - apartment cities, five to eight storeys tall, built around courtyards on enormous blocks, owned by rentier corporations or landed estates and inhabited overwhelmingly by tenants.

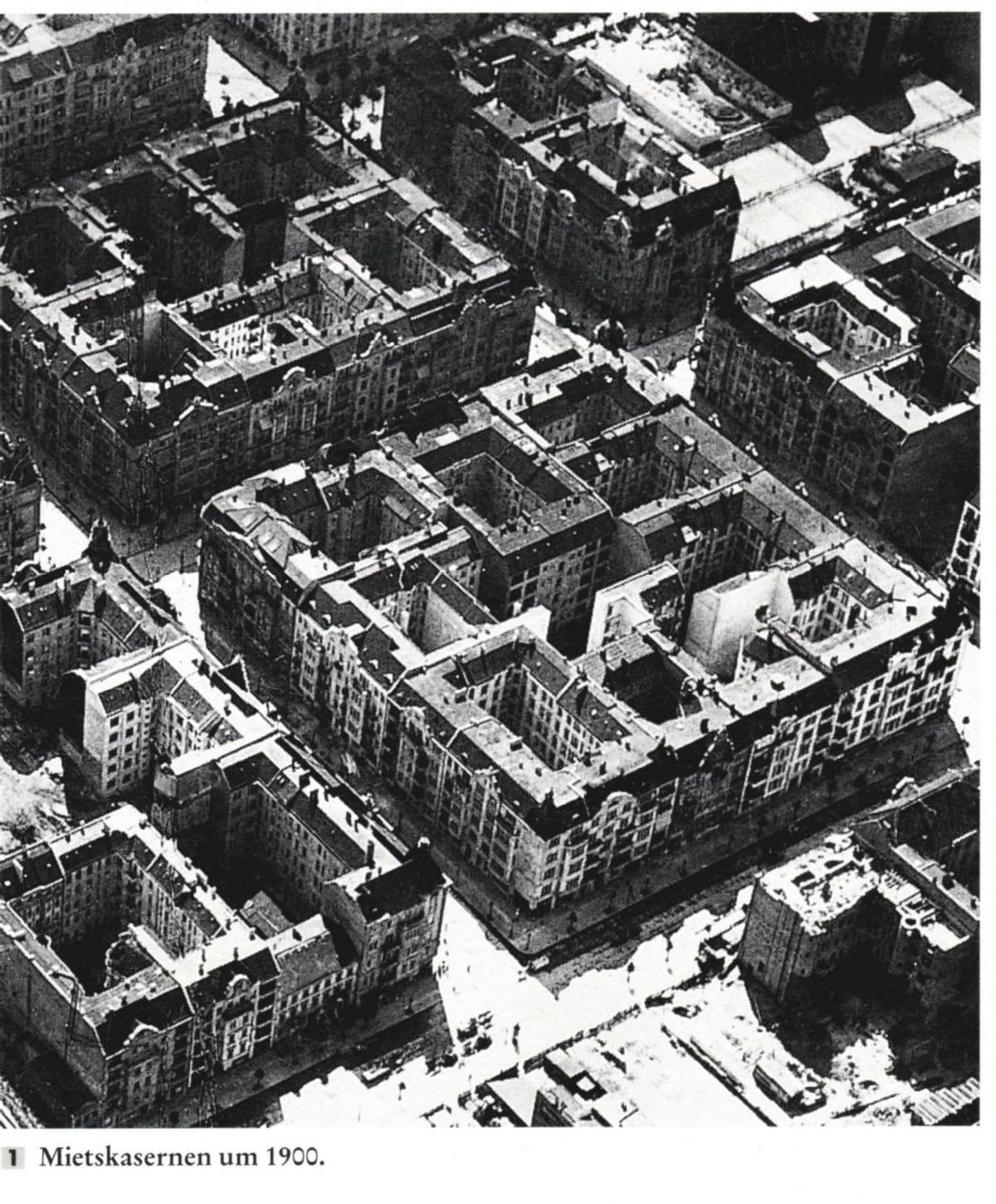

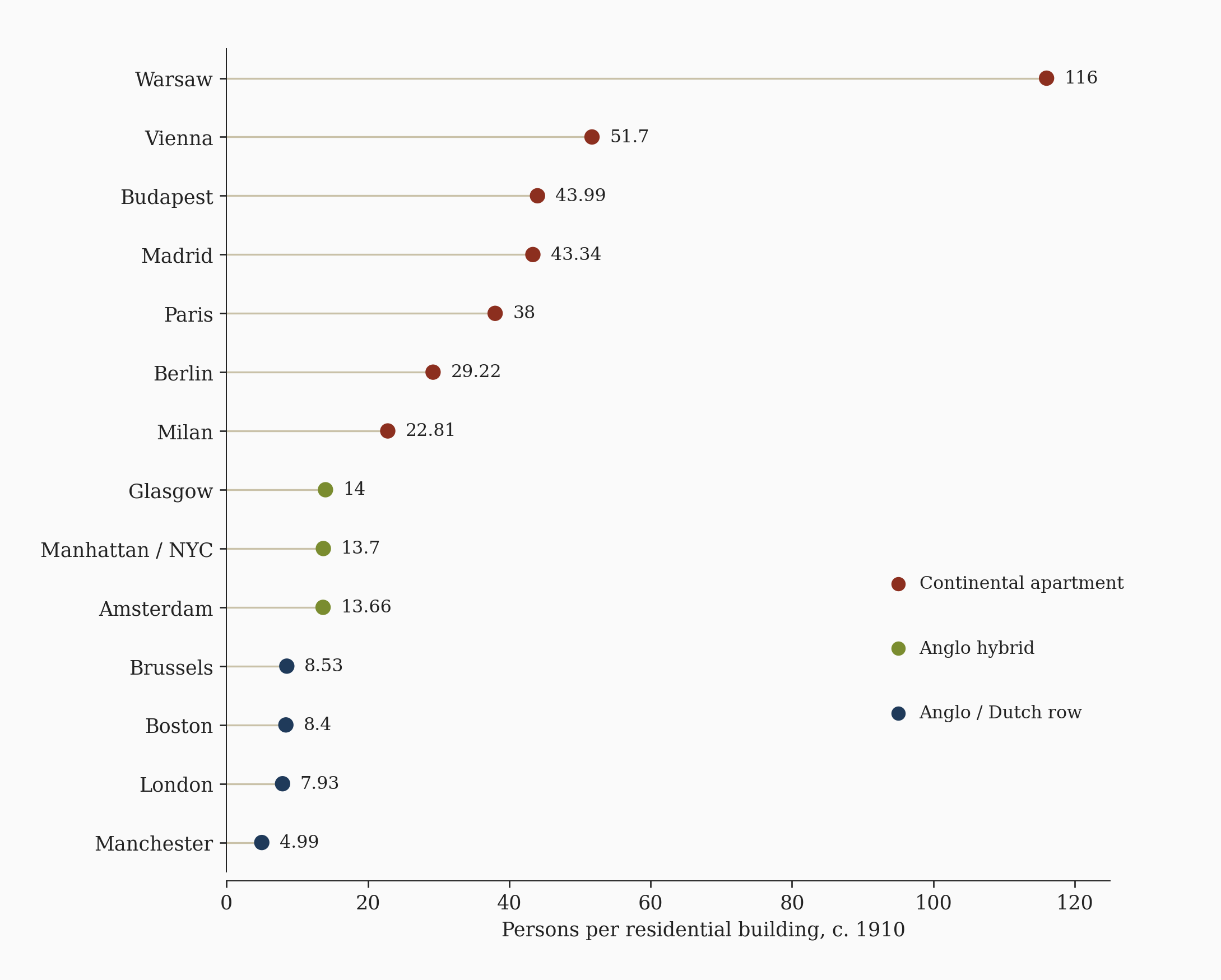

The single best comparative measure of the gap comes from a cross-section of 1,095 cities across 27 countries, drawn from late-nineteenth and early-twentieth-century census data.1 Measured as persons-per-residential-building, English industrial cities had an urban density of roughly 5 to 6, greater London and Belgian cities around 8. The Dutch were already a little higher (Amsterdam 14, Rotterdam 11). Paris, on the other hand, with 38 persons per residential building sits at the higher end. The Central European capitals were higher still: Vienna 52, Budapest 44, Madrid 43, Berlin and Hamburg around 29 city-wide but with individual inner districts reading in the high 50s. At the extreme, Warsaw climbed to 116 persons per residential building - a number that is hard even to picture. On this morphological measure, the Continental and the Anglo-Dutch sides were separated by a full order of magnitude.

Of course the pattern was not absolute and the exceptions matter. There were apartments in the Anglo world - Manhattan’s Lower East Side dumbbell tenements (about 70% of New York’s five-borough population lived in tenements by 1900),2 Glasgow’s sandstone tenements, parts of Chicago and Boston. Conversely, there were row houses on the Continent - the bourgeois working-class quarters of Lyon, certain German industrial towns, the Brussels and Antwerp town house. Each of these exceptions has a specific mechanism, and we’ll work through them as we introduce our framework revealing the forces producing urban morphology.

A second dimension is worth introducing here. Around 1900, essentially everyone in both kinds of city was a renter. Three-quarters of London households were tenants in the early-modern period,3 reaching further up to 90% rental into the 1910s.4 On the Continent the rental share was higher still - over 90% in Wilhelmine Berlin and fin-de-siècle Vienna. So the contrast that matters is not rental Continent versus owner-occupier Anglo, but the form of the development and the capital structure that owned it.

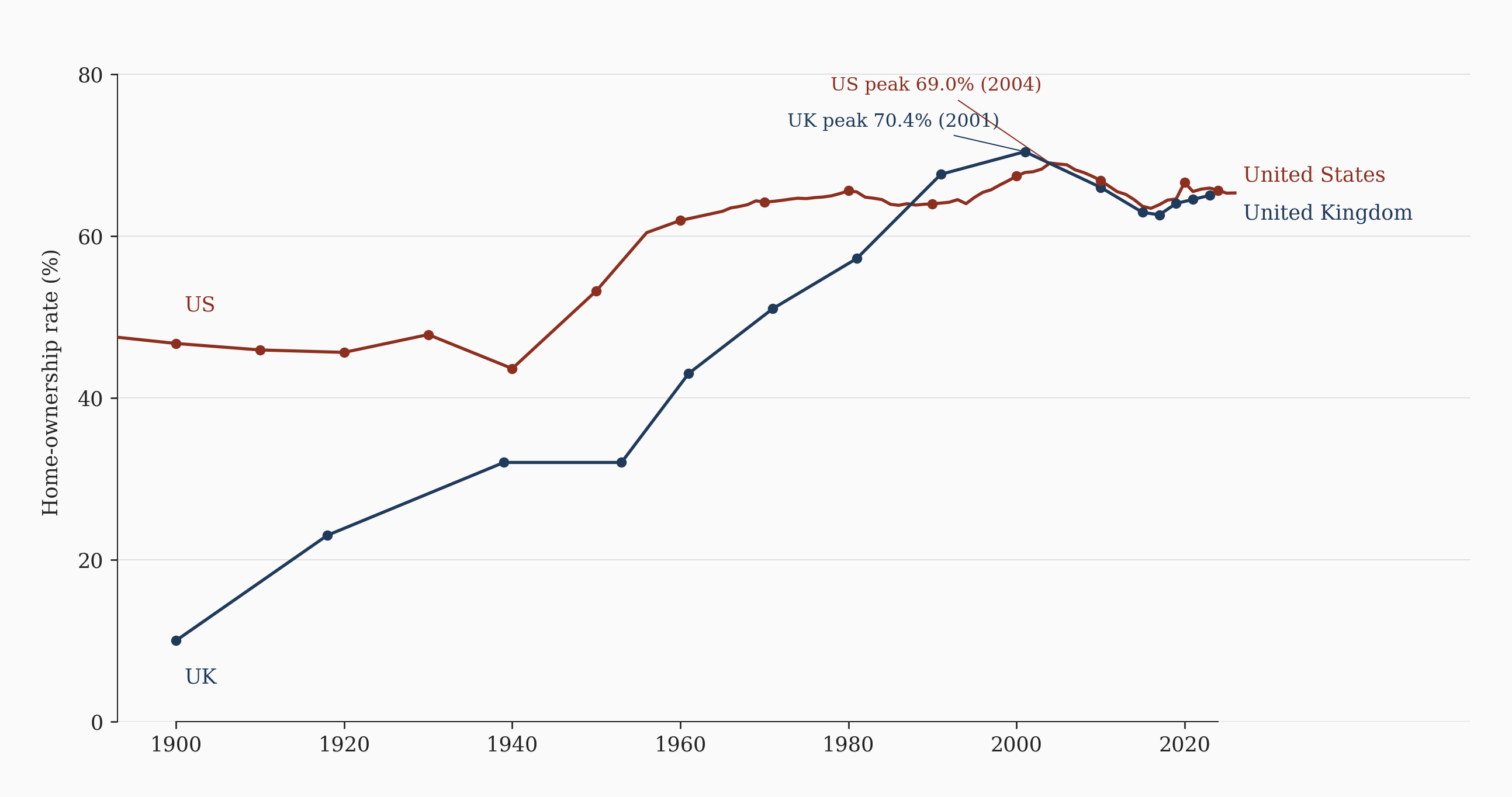

The twentieth century rearranged the tenure pattern twice. Between 1918 and the early 2000s the Anglo world became majority owner-occupier (the US peaked at 69% in 2004; the UK at 70.4% in 2003). The Continent retrofitted owner-occupation onto apartments through new horizontal-property laws - the Italian condominio of 1934, the French copropriété of 1938 and 1965, the German Wohnungseigentumsgesetz of 1951, Spanish propiedad horizontal of 1960, Swiss Stockwerkeigentum of 1965, and the Eastern European mass privatisations after 1990.

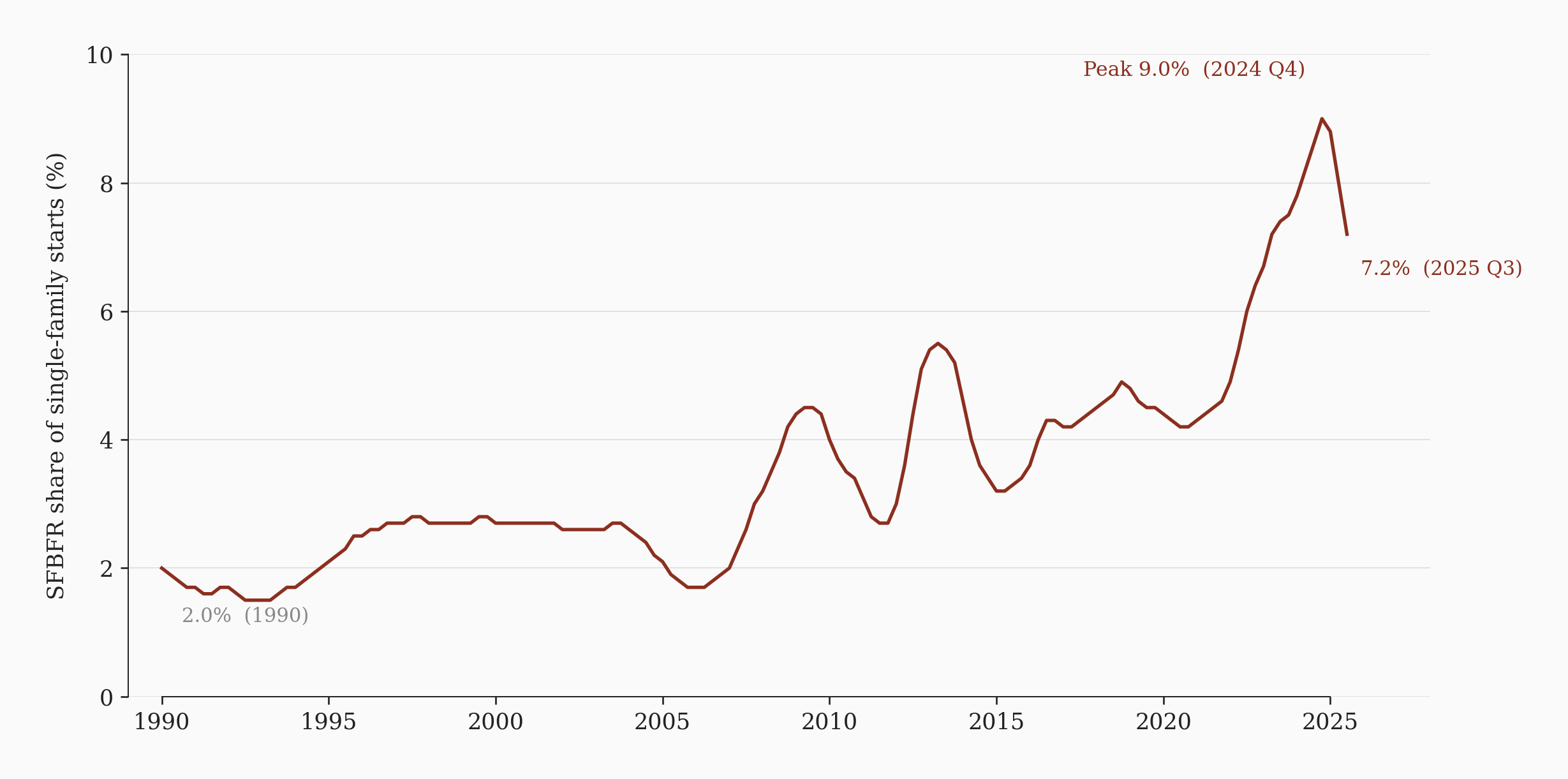

From the 2010s the institutional rental form has been returning. By 2022 the four largest US single-family-rental landlords together held more than 200,000 homes; in 2011 no single firm held more than 1,000. Build-to-rent has risen from under 2% of US new single-family starts in the 1990s to over 7% today, with at least 68,000 new BTR starts in 2025 alone.5 In Europe, Blackstone, Vonovia, Akelius and Heimstaden together own hundreds of thousands of apartments across Germany, Sweden, the Netherlands and Spain. The first major American institutional rental construction wave since 1929 is underway. The pace shows up in the construction statistics.

My aim across Parts 1-3 of this series is to build a political-economic model of urban form: a model that explains what gets built in a city, and who ends up occupying it, from a set of form-side and use-side variables. On the form side are the rules, institutions, and financial structures that determine what kind of building can be produced: plot structure, ownership law, building codes, lease length, credit, developer scale, and regulatory envelope. On the use side are the variables that determine who occupies that form: household structure, tenure, rent levels, income distribution, migration, demographic pressure, and the relationship between land, debt, and income.

The ambition is that the same framework should be able to take Paris in 1865, Berlin in 1900, Madrid in 1860, London in 1820, Berlin’s 1853 Bauordnung, Moscow under dolevoe stroitelstvo, Singapore HDB, Dubai Marina, or Phoenix build-to-rent, and, when plugged the relevant parameters, return not only the morphology visible on the ground, but also the tenure structure that inhabits it. In other words, it is a parameterised model of urban production, with named institutional inputs. The same variables should explain both nineteenth-century outcomes and contemporary cases. But before we can build that model, we need to clear the ground. We need to understand the forces and mechanisms that shaped these cities, and we need to examine the standard explanations for one of the most striking facts in modern urban history: the deep split between Continental Europe and the Anglo world in the urban form that occupies the ordinary fabric of their cities. Why did one world produce apartment blocks, perimeter blocks, rental tenements, and vertical subdivision, while the other produced terraces, row houses, suburbs, leasehold estates, and later single-family sprawl?

Why the usual answers fall short

The standard accounts of why Paris ended up apartments and London ended up rows fall into a handful of explanations, each commonly invoked in popular and academic writing: Walls and fortifications forced the Continent up; industrial pressure on scarce urban land drove density vertical; national character - sociable French, private British - produced its own physical taste; long-leasehold tenure made small plots inevitable in England; fragmented ownership couldn’t aggregate the parcel sizes Haussmann needed. Each of these accounts has merit and some explanatory power, but runs into an important case it cannot explain.

The walls thesis. Continental cities were ringed by walls, on the popular telling, until late in the nineteenth century, scarcity drove up land prices inside the walls, and thus the only economical answer was to build up. This intuition was voiced by nineteenth-century reformers themselves - Martin Nadaud told the Chamber of Deputies in 1882 that the Thiers Wall had left Paris “choking in her straitjacket”, and a residue of the argument survives in handbooks of European urban history.6

The trouble with this story is that the contrast it needs, walled Continent vs. unwalled Anglo cities, doesn't hold. English cities had largely shed their medieval walls by 1700 - London’s wall was already a relict feature by the Restoration, gates were demolished in 1760, and Manchester, Birmingham and Liverpool grew through the eighteenth century without any fortified perimeter. If walls had been the cause of apartment morphology, England should have produced row houses, which it did, while the Continent should have produced apartments only while its walls still stood, which it didn’t - the Mietskaserne and the Haussmannian immeuble arrived after the Continental walls were down. The dating is wrong in both directions. Archival reconstruction of German defortification finds that the great majority of German cities had pulled down their walls long before the apartment-block boom - by 1816, around 60% had already done so, and in Berlin the walls came down in the 1730s.7 Industrialisation in the canonical sense did not begin until decades after the walls were already gone.

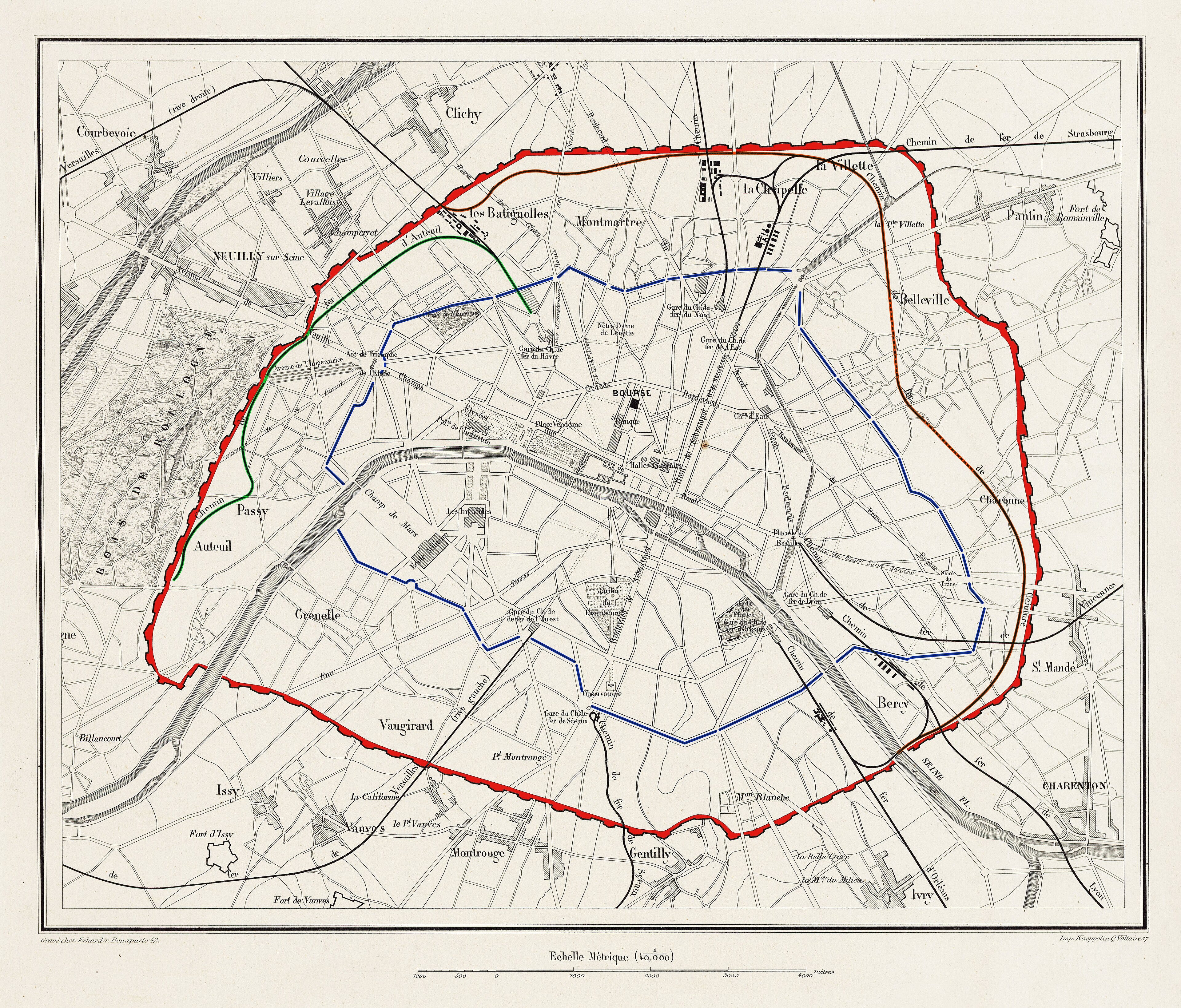

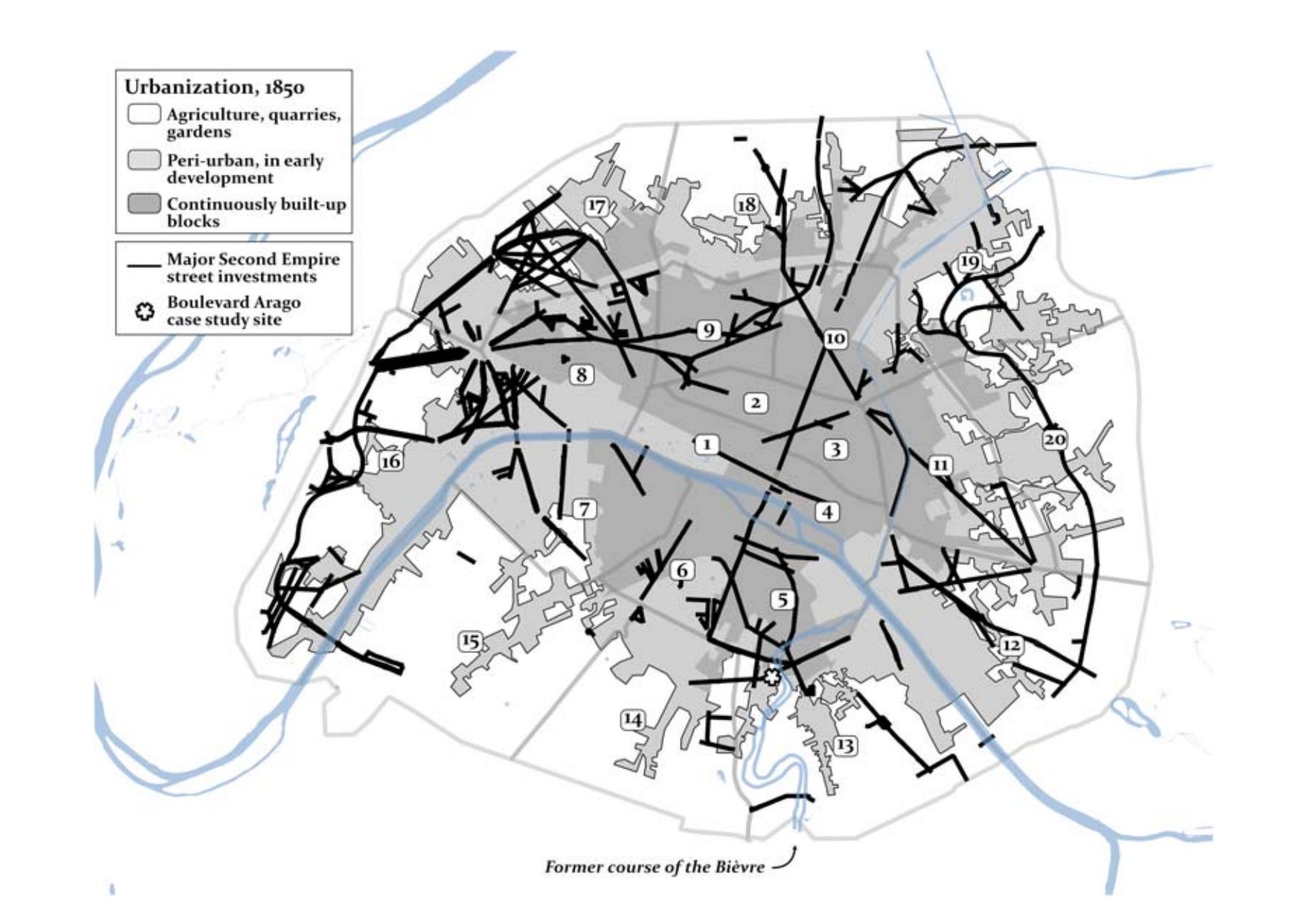

A recent reconstruction of where Haussmann’s new boulevards actually ran shows that about two-thirds of the new boulevard length passed through peri-urban land outside the inner city - farms, quarries, gardens - and another tenth through fully agricultural country.8 The Paris that Haussmann built was built mostly beyond the walls, not constrained inside them. The Hobrecht plan extended Berlin into open Brandenburg country, far past any meaningful fortification. If walls had been the cause, German defortification should have unleashed row-house sprawl rather than Mietskasernen.

The industrial-pressure thesis. This story goes something like this: industrial growth drove populations into cities, cities had limited land, vertical density was the rational response. The strongest counter-evidence to this is that British cities had the same industrial pressure and did not produce apartments. Bethnal Green, Whitechapel, the back-to-backs of Liverpool and Birmingham, the working-class districts of Manchester all reached densities that rivalled Berlin and Vienna - but in row-house form.

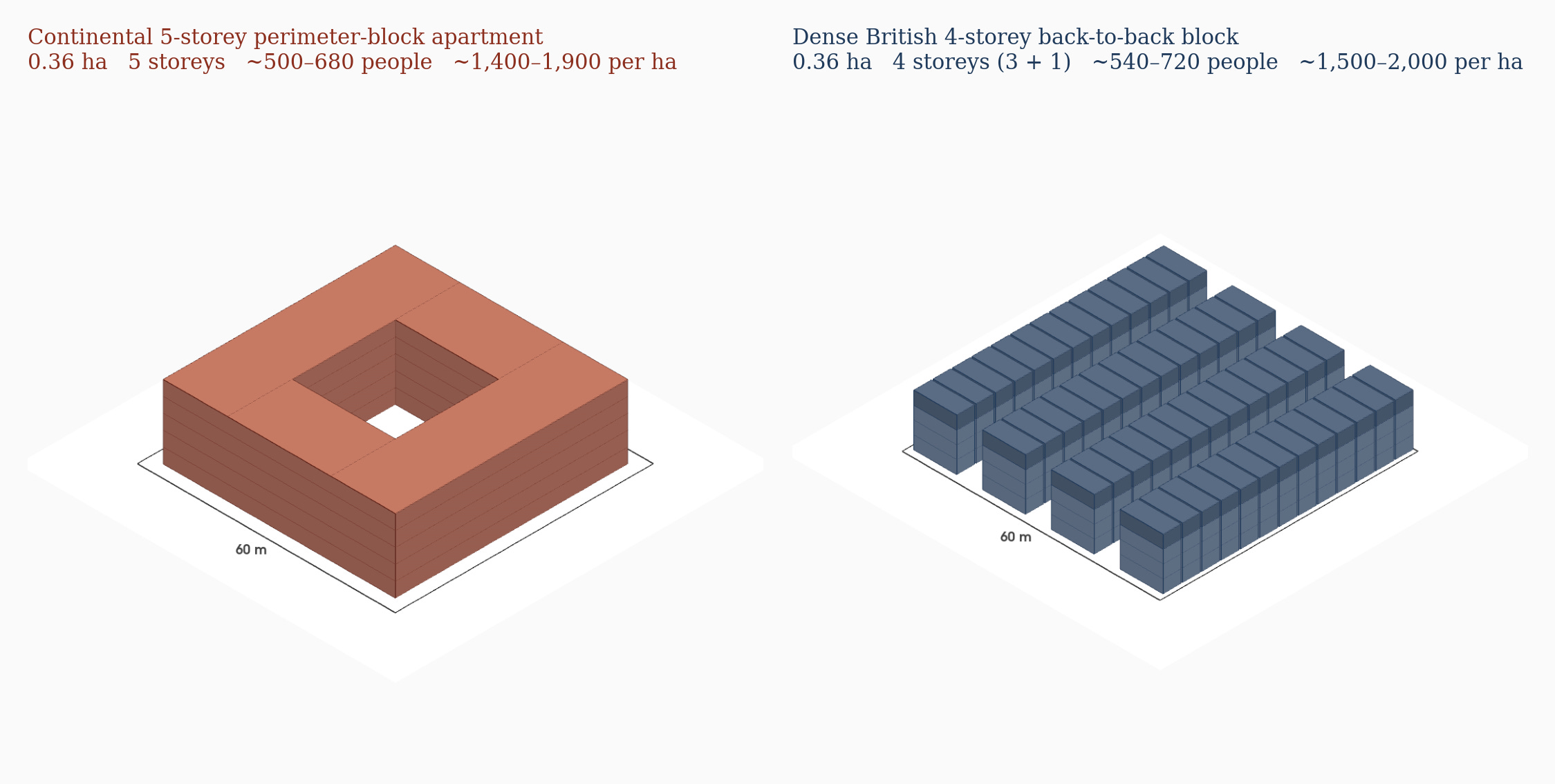

It is worth seeing this directly. On a 0.36-hectare urban block, a typical Continental five-storey perimeter-block apartment - a single building wrapped around a central courtyard, in the form documented for Paris Haussmann, Vienna and Madrid - held around 500 to 680 people at late-nineteenth-century working-class occupancy, about 1,400 to 1,900 persons per gross hectare. The same block laid out as a British back-to-back district, about a hundred narrow back-to-back houses in four parallel rows separated by narrow streets, held around 500 people at three storeys, the standard Leeds and Birmingham form. Add a fourth storey, as Liverpool's central court housing and the older East End working-class terraces routinely did, and the same 100 dwellings carry roughly 540 to 720 people, about 1,500 to 2,000 per hectare - squarely in the same band as the typical Continental five-storey apartment, sometimes a touch above when British occupancy ran more cramped per person.

The British row-house regime sat in the same density band as the typical Continental apartment city: lower at two or three storeys, in the same range at three to four. Only the densest Continental form - the six-storey Berlin Mietskaserne with its tight Bauordnung courtyards - ran significantly higher, around 2,200 per hectare, and the unregulated British slum extreme of the Old Nichol type climbed even higher by sheer overcrowding. What matters is that whatever produced the morphological split between an apartment city and a row-house city, it was not density. It has to come from somewhere else.

The cultural thesis. A version one often meets in middlebrow journalism reads the divide as a question of taste: the French live communally, the British live privately, and the buildings follow the temperament. The thesis is attractive but it does not survive its counter-cases. Belgium and France operated under the same Napoleonic Code from 1804 and yet produced predominantly row houses and apartment blocks respectively - same legal substrate, same broadly Catholic civil-law culture, yet different urban forms. Brooklyn and Manhattan operated under the same New York statutes and produced row houses and tenements within walking distance of each other. No theory of national character survives these simple counter examples.

The tenure-form thesis. Richard Rodger’s reconstruction of British housing 1780-1914 reports a careful within-Britain comparison that ought to have killed the freehold-vs-leasehold story. Freehold-dominated Leeds (with its prominent middle-class suburb at Headingley) and overwhelmingly leasehold Birmingham (with Edgbaston) produced almost identical row-house middle-class suburbs.9 Tenure form, taken on its own, does not predict morphology - two cities in the same country with opposite tenure systems produced the same kind of street. The framework I will lay out captures this case by treating tenure as a use-side variable that interacts with the form-side capital stack rather than as an independent driver of form.

The fragmented-ownership thesis. According to this account, fragmented ownership produces small terraces of four to eight houses, while larger holdings allow more consolidated development.10 This is a real argument, and it lights up one of the things going on. But it also fails as a master variable: Brooklyn was fragmented and produced row houses; Vienna’s pre-1848 Vorstädte were also fragmented among petty noble and monastic landlords and yet produced apartment buildings. The framework I will propose will attempt to explain Vienna by separating the scale of the city’s overall ownership (fragmented in both Brooklyn and Vienna) from the scale of the actor at any single parcel (the Viennese Vorstadt landlord controlled a contiguous courtyard parcel; the Brooklyn freeholder controlled a frontage plot). The same concept - fragmentation - operating at two different scales, producing opposite outcomes.

The zoning thesis. The contemporary Anglo-American argument points at the American single-family-detached zoning regime that emerged after 1916 and made it illegal to build apartments in most American suburbs.11 As an account of why post-1916 American suburbs are detached-house cities, this is empirically true and matters. As an account of why London, Manchester, Liverpool and Brooklyn were already row-house cities in 1850 - two generations before the first US zoning ordinance - it cannot do the work. American zoning rules out the apartment in places that already weren’t producing it; the morphological split is older than the law. Zoning enters our framework as one of the levers under the building-code variable. It is a late-arriving regulator of a phenomenon whose original cause lies elsewhere.

Each of the above accounts grabs one variable and treats it as primary. The mechanism I aim to propose treats them together within an interconnected hierarchy, and once that hierarchy is in view, I hope to arrive at a model with sufficient explanatory and predictive power.

The Framework

The architecture of the urban morphology model is hierarchical. At the bottom sits the inheritance regime: civil-law forced partition on the Continent versus common-law strict settlement in England. This is the substrate: a society’s standing instruction to its propertied class about what kind of capital it is allowed to hold and pass on. From that substrate three enabling conditions of construction follow within a form-side equation - who draws the block, what the building code permits on it, and at what scale the developer who builds on it is allowed to operate. The enabling conditions are funded by two financing flows - a builder-side credit channel that pays for the construction and a buyer-side credit channel that funds the eventual occupier. A political constraint - the rent-control regime - sits across the top of the stack and decides what return the building can earn once it stands.

Urban Morphology = F( Block size × Building code × Developer scale × Builder-side credit × Buyer-side credit × Rent-control regime | Inheritance regime )

The use-side equation hangs off the same inheritance substrate at its other end: the legal regime that tells the propertied class what kind of capital to hold also tells the dominant household what kind of asset to hold, and combines with tenure law and labour-market structure to decide who lives in what gets built. Inheritance is one variable; its two appearances at the bottom of the form equation and the bottom of the use equation reflect two scales of action that the same legal regime governs at once - the constitutional and the household.

Urban Inhabitation = U( Tenure law × Labour-market structure | Inheritance regime )

With that architecture in view, let us introduce the form-side variables in the order they operate, from the planner’s pencil to the politician’s regulation:

• Block size - how big is the parcel of land on which a single development sits, and who draws it. The main distinction we will return to is that in Continental cities the state draws the block, while in Anglo cities the aristocratic estate parcels it out.

• Building code - the rules that decide what can be built on the parcel, including height, courtyard minimums, and lot coverage. For example, Berlin’s 1853 Bauordnung permitted six storeys with a 5.34-metre courtyard; London’s Metropolitan Building Acts after 1844 capped heights and required setbacks.

• Developer scale - the size of the firm that does the actual construction. While a continental rentier-corporation could finance and build a six-storey apartment block, a British master tradesman could finance and build three or four row houses at a time.

• Builder-side credit - the credit channel that funds the construction. On the Continent, Prussian Pfandbrief-style covered bonds: long-duration bonds issued by a mortgage bank against a ring-fenced pool of urban-property loans, sold to bourgeois savers, with the bondholder paid out of the rental flow of the underlying buildings. On the Anglo side, improved-ground-rent capitalisation: short-term lending against the present value of the rising ground rent the completed houses will generate, advanced plot by plot rather than building by building.

• Buyer-side credit - the credit channel that funds the eventual occupier of the building. Building societies, savings-and-loans, FHA, Bauspar, CPF - institutions that aggregate household deposits to lend back to households as mortgages.

• Rent-control regime - the political constraint on what rent the building can charge once it exists. The broad pattern was a light regime before 1914 almost everywhere, tightening sharply after the wars, and relevant again now.

And the use-side variables in the equation that decides how the form is inhabited:

• Tenure law - what can legally be owned. An important case we will discuss: horizontal-property law makes individual apartment ownership possible, while its absence requires the apartment building to be rented whole.

• Labour market - whether tenants converge on a few-per-house pattern (middle-class) or a many-per-room pattern (immigrant tenement). For example, the same row house can house one Brooklyn family or twelve.

• Inheritance regime - as mentioned above, this regime determines if a household chooses (or has chosen for it by law) whether to hold its wealth in liquid divisible form or in dynastic landed form.

The framework’s claim is that the Continental apartment city of 1850-1914 is the case in which the form-side variables fall on the apartment side and the use-side variables produce mass rental, producing the apartment block morphology. The Anglo-Dutch row-house city is the case in which they fall the other way, producing the row-house morphology. The interesting cases - Glasgow, Brooklyn, Buenos Aires, Vienna before 1848, Amsterdam - distribute the variables across columns and produce hybrid morphologies. Glasgow is the cleanest illustration: Scots feu tenure (an alienable perpetual-rent freehold rather than the English 99-year leasehold), Scots inheritance law and the city’s small jobbing builders sit on the row-house side of the table, while ground-annual capitalisation and the sandstone block sizes negotiated by the Victorian estate offices push the form upward into the four-storey tenement. The result is an apartment morphology grown out of row-house legal material. Part 3 plugs the variables in for each of these hybrid cases explicitly, showing for each city which variables fall on the apartment side and which on the row-house side. The same form and use equations account for the contemporary cases of Parts 2 and 3 as well: Soviet mikrorayon, post-Soviet dotted high-rises, Hong Kong, Singapore, Dubai, the Sun Belt build-to-rent suburb.

The rest of Part 1 begins at the bottom of the hierarchy - the inheritance variable, in its substrate role - and walks one variable up. Part 2 carries the chain through Berlin’s particular history and turns to the two credit channels; it is also where a deposit-based versus bond-based mortgage-institution typology gets unpacked alongside the builder-side and buyer-side channels, and where the post-war comparative-political-economy literature on the homeownership / welfare-state trade-off connects to the tenure flip.1213 Part 3 plugs the variables into the contemporary cases.

Inheritance law and the kind of capital it forces a society to hold

The inheritance regime is the layer most often skipped in popular accounts. It matters because an inheritance regime is, structurally, a society’s instruction to its propertied class about what kinds of assets it is allowed to hold and pass on. The instruction differs sharply between civil-law Continental Europe and common-law England, and the difference is the bedrock on which the form and use equations both rest.

The French regime: forced partition

The popular story is that the French Revolution and Napoleon imposed forced partition - the rule that estates must be divided in cash-equivalent shares among all the children - out of egalitarian principle. The Code Civil of 1804 set the rule explicitly: a father with three or more children could freely dispose of at most a quarter of his estate by will (the quotité disponible); the remaining three-quarters had to pass in equal shares to the children. The function of the rule, however, was older and more specific than equality. It was a deliberate political dismantling of the institutional infrastructure of the ancien régime aristocracy.

Pre-revolutionary France was a legal patchwork. North of a line running roughly from the Loire estuary to Lake Geneva, customary law (coutume) prevailed, in which testamentary freedom was limited and customary partition rules applied unless the family used elite-preservation devices. South of that line, the Roman law of testamentary freedom (droit écrit) survived from the Theodosian Code and gave nobles the legal tools to bequeath whole estates to a single heir.14 In both north and south, the ancien-régime aristocracy used two specific instruments to preserve estates intact across generations - substitution fideicommissaire, a directive that an estate pass intact through a sequence of named heirs without alienation, and the majorat, the entailed estate attached to a noble title.

The Constituent Assembly’s decrees of March 1790 and April 1791 abolished primogeniture and substitution fideicommissaire together. The Code Civil of 1804 generalised the abolition into a permanent constitutional immunisation - what historians have called the “Great Demarcation” of property from political power that defined the revolution’s deepest project.15 The réserve héréditaire (the three-quarters of the estate that must pass to the children) is the operational core of this immunisation: a father cannot bequeath the bulk of his estate to a single heir even if he wants to. Napoleon’s majorats impériaux of 1808 briefly reintroduced an entail for the new imperial nobility, but the Restoration Charter of 1814 and the law of 12 May 1835 abolished those majorats as well. By the mid-nineteenth century the réserve was uncontested.

The downstream consequence of this regime is the decisive one for our story. A seigneur under the ancien régime could leave his domaine - a contiguous, named, dynastically transmissible tract - to his eldest son, and the domaine would continue to function as the territorial base of the family. Under the Code Civil he could not. The estate had to be divided into cash-equivalent shares, which meant either physical subdivision (selling pieces to outside buyers and distributing the cash) or formal partition (each heir receiving a defined parcel). Within a generation the dynastic domaine dissolved into smaller plots in scattered hands. The French aristocracy lost the territorial substrate of its political weight, exactly as the revolutionaries intended.

Within a city the same logic applied. A bourgeois Parisian holding a building under the Code Civil could not pass the building intact to one heir. He had to leave four children four cash-equivalent shares - which in practice meant either that the children sold the building to a third party and divided the cash, or that the building entered the hands of an institutional vehicle that owned it whole and issued the heirs four fungible shares in the vehicle.

That institutional vehicle was the Compagnie Foncière - the joint-stock urban property company. The four heirs each held, say, 25 shares in a company that owned 40 buildings. The same arithmetic of fractional ownership that would have been absurd applied to a single building (a quarter of a particular staircase, a quarter of a particular roof) was rational at the company level - 25 shares in a 40-building portfolio is a tradable, mortgageable, marketable claim, valued daily, with a board of directors making the operational decisions on behalf of fractional shareholders. What made these otherwise absurd fractional claims workable was the governance layer the company supplied. A board of directors translates fractional shareholdings into coherent management of the underlying asset, and the shareholders can sell their fractions to a willing buyer rather than physically dividing the building. The institutional response to the réserve héréditaire was therefore the bourgeois rentier corporation, holding apartment buildings as undivided assets on its own books and offering its shares to bourgeois savers under the same partition rule.

The English regime: strict settlement

The English aristocracy in the seventeenth and eighteenth centuries built a different machine, the strict settlement. This was an elaborate trust device. The present holder of the estate was a “tenant for life” - entitled to the income of the estate during his lifetime but with no power to sell the underlying freehold. The eldest son was a “contingent remainderman”, who would inherit the same life-tenant position on his father’s death. The grandson was the next contingent remainderman, and so on. The present owner could not, by his own act, alienate the estate. Only a private Act of Parliament could break the settlement and free the freehold for sale.

The institution sat at the centre of the political settlement that emerged from 1660-1688. The Restoration and the Glorious Revolution stabilised a bargain between the Crown and the landed class. The landed class kept its estates intact across generations as the territorial basis of its political weight in Parliament; in exchange, it accepted constitutional monarchy, parliamentary supremacy and gradual reform. Strict settlement was the institutional infrastructure that contributed to preventing an English 1789 - the aristocracy had a permanent territorial base, so a revolutionary expropriation of noble land was politically unnecessary (they could be managed within Parliament) and practically impossible (the trust law was robust enough that even Parliament needed a private bill to break it).

Why did aristocrats accept that only Parliament could break their settlements? The answer is partly self-protection across generations and partly political. Strict settlement was, in the eighteenth-century sense, an insurance policy against one’s own descendants. The “tenant for life” of a great estate held the income but could not sell the freehold or even grant a building lease longer than 99 years on his own authority. The eldest son in the next generation took the same restricted position. Any father in the family could therefore be confident that his grandson would inherit an estate roughly the same size as the one his own father had handed him - even if his son turned out to be a gambler, a drinker, a sectarian enthusiast, or simply a fool. The fear of a profligate or extravagant heir is the recurring justification in eighteenth-century conveyancing manuals and family settlements: the family bound itself to the trust precisely because the family did not trust each of its own future members.

Why was Parliament willing to be the bottleneck? Because Parliament was the landed interest. The same families who held the great estates sat in the Lords and dominated the Commons. Asking Parliament to break the entail was, in effect, asking one’s peers to consent. The reconstruction of the parliamentary record shows that this consent was given liberally where the purpose was development that increased the estate’s long-term value - urban building leases, drainage improvements, canal access, railway crossings. Parliament was not obstructing the great estates; it was performing the trust function the family wanted performed. The 99-year cap, the private-act mechanism, and the Estate Acts together produced exactly the outcome the landed class had bargained for in the constitutional settlement: an aristocracy whose territorial base survived 1789 because no internal mechanism inside Britain could expropriate it without parliamentary consent, and parliamentary consent was theirs to give.

Parliament supplied the release mechanism that kept the system from seizing up. Between 1600 and 1830 it passed roughly 3,500 Estate Acts - private bills that broke specific entails to release specific parcels for specific purposes, very often urban development.16 The Bedford Estate’s release of land for Bloomsbury, the Grosvenor Estate’s release of Mayfair and Belgravia, the Foundling Hospital Estate, the Mercers’ Company’s Stepney leases, the Portman and Cadogan estates - every great London estate in our story is a piece of land that was once entailed, then unfrozen by an Act of Parliament under strict settlement, then leased out plot by plot to small builders.

A natural question arises: if aristocratic land was frozen in dynastic trusts, where did England's investable capital come from? England in the nineteenth century plainly did have liquid divisible capital - the joint-stock railway, the foreign investment trust, the colonial development bond, Consols and the Funds. Strict settlement bound the landed aristocracy’s estates, but it did not touch the merchant, banking, and joint-stock wealth held in the City of London - the square-mile financial district whose institutions had grown alongside, and largely separately from, the country estates since the seventeenth century.17 The two pools of capital developed in parallel rather than meeting in the same channel. Aristocratic urban land in London flowed into long ground leases on the Bedford, Grosvenor, Portland, and Portman estates under the strict-settlement constraint, while bourgeois City capital went into railways, foreign loans, Indian and Egyptian bonds, and Consols.

The follow-on question is how the major early-modern infrastructure projects in Britain - canals, factories, the first railways - were financed if aristocratic land was tied up behind strict settlement. The answer is that strict settlement constrained aristocratic land but did not freeze it absolutely, and in any case it applied only to the great dynastic estates, not to all English land. In the eighteenth and early nineteenth century, land - both settled aristocratic land and unsettled fee-simple land held by smaller gentry and manufacturers - was used as security for industrial loans, but at the level of the individual landed industrialist and his country bank, not through a national mortgage-bond market. The Duke of Bridgewater pledged part of his estate to borrow the £25,000 that built Britain’s first canal in 1763, and used his political connections to obtain four Acts of Parliament that gave the canal company statutory powers to compel other landowners along the route to sell. Matthew Boulton sold and mortgaged most of his land, then raised £28,000 by pledging his wife's property to finance his first large factory in Birmingham. Jedediah Strutt raised loans against his farm to develop the stocking-frame whose profits later helped fund Arkwright's water- and steam-powered textile factories. Examples abound. By one nineteenth-century computation, two thirds of the capital available before the spread of large private banks existed in the form of real estate rather than financial securities; as late as 1832 land still represented half of all British wealth.18

What Britain did not develop was the institutional layer above the country bank - the standardised, bond-issuing mortgage bank that could pool mortgages on land and buildings and sell long-duration paper into a capital market. That layer is what the German states had built in the Pfandbrief tradition and what France built around the Crédit Foncier in 1852; Britain built no equivalent. When the moment came that might have called for it - the railway boom of the 1830s and 1840s - the railway companies were raising capital on a scale that no land-pledge country-bank channel could have supplied, and they raised it instead by issuing shares and bonds against projected toll, fare and freight receipts on the joint-stock model, accelerated by the Limited Liability Act of 1855 and the Joint Stock Companies Act of 1856.19

On the Continent the bond-mortgage layer did get built. The Prussian Landschaften, beginning in the 1770s after the Seven Years’ War, were cooperative mortgage associations that issued covered Pfandbriefe against East-Prussian Junker estates and re-sold the paper into Berlin and Hamburg.20 France's Crédit Foncier, founded in 1852 under the Second Empire, took bond-financed mortgage credit national, and by the late 1860s had become central to the financing of Haussmannian construction - holding some 398 million francs of City-of-Paris paper by 1868.21 Spain's Banco Hipotecario de España of 1872 then took the same architecture into a Madrid that had been opened up by the liberal desamortización of 1836-1855.22 The shared institutional feature here is the bond-issuing layer above the country bank.

The Continental world had no bifurcation of land-based and merchant capital as was the case in England. After the réserve héréditaire, disentailed land and bourgeois capital met in the same place - the urban block - and the apartment building was the meeting room.

An educated reader will rightly object that English gentry land was not bound by strict settlement, and that significant urban land was held in fee simple outside the great dynastic estates. The objection holds. Inheritance regime is the substrate, not the whole mechanism. The natural experiment we can look for is internal to England itself: Leeds and the West Riding were freehold cities with no dominant aristocratic ground-landlord, yet they produced the densest back-to-back terraces in Britain. This is well documented: “serious housing deficiencies were not confined to one type of tenure or location. Poorly drained areas were developed for industrial purposes or working-class housing irrespective of who owned the land, how concentrated the ownership was, or the nature of the tenure,” and “freehold-dominated Leeds and overwhelmingly leasehold Birmingham produced almost identical middle-class suburbs.”23 The strict settlement of the great estates was therefore one filter among several, not a single sufficient cause; the row-house outcome was overdetermined by a stack of mutually reinforcing institutional conditions, which this article series will work through in turn. Inheritance comes first because it is the deepest layer - the legal architecture of property itself - but it does its work only in combination with what follows.

A paradox worth pausing on

Read against each other, the two regimes seem to produce the opposite of what they should. England’s strict settlement preserved aristocratic estates intact across generations - the Bedford and Grosvenor freeholds in 1900 looked very much like the Bedford and Grosvenor freeholds in 1700. The Revolution and Napoleonic inheritance law in France weakened the aristocratic estate system in a different way: feudal rights were abolished, roughly 6.5% of French territory was auctioned off from confiscated Church land between 1790 and 1796, another 3.5% from émigré property between 1793 and 1815, and equal-shares inheritance under the Code Civil made large dynastic landholdings harder to preserve across generations than they had been under the ancien régime.24 By the late nineteenth century the aristocracy still owned land - in some regions, a great deal of it - but the dynastic domaine as a coherent territorial unit had been broken down into smaller, separately-titled parcels that often passed through the market between generations.

Thus, the Anglo regime kept estates large, whereas the Continental regime did not. And yet the Anglo regime produced cities built on small plots - Bloomsbury’s 22-foot frontages, the Mercers’ Company’s six-houses-per-builder, the Brooklyn brownstone - while the Continental regime produced cities built on large blocks: Haussmann’s superblock-scale apartment buildings, the Hobrecht Plan’s five-hectare blocks in Berlin, Cerdà’s 113-metre square in Barcelona. How can holding large estates intact produce small development parcels, and breaking estates up produce large development parcels?

The resolution is in the legal monetisation routes each regime made available. The English aristocrat under strict settlement could not sell his freehold - he was a life tenant under his own family’s trust. He could grant building leases, but conveyancing practice as it had evolved since the early-eighteenth-century building booms in London and Bath limited the maximum term to 99 years on his own authority. The first 99-year building lease in London was granted on the Bedford Estate at Bedford Square; by 1765 the Bath Corporation was granting 95% of its leases on that term. The Settled Estates Act of 1856 and the Settled Land Act of 1882 later codified this conveyancing practice into statute; longer leases required a private Estate Act of Parliament.25 The only available counterparty for a building lease was the master tradesman with three to six plots of working capital - a class of builders that had emerged out of the British construction apprenticeship system in the eighteenth century and that we’ll look at directly in a moment. The aristocrat’s estate stayed large, but the legal instrument forced its urban development to come out small.

In France, by contrast, the réserve héréditaire freed aristocratic land into a market of bourgeois proprietors with fungible savings. The state inherited the urban-planning role that the aristocracy had vacated, and the state then exercised it at a much larger scale than any private aristocrat would have. Haussmann’s prefecture, Hobrecht’s commission in Berlin, Cerdà’s Barcelona ensanche, Castro’s Madrid - these are state actors drawing blocks at a scale that no aristocratic estate office had ever attempted. The estates were broken up but the development parcels were not. Instead, they were drawn by the new state.

So the apparent paradox is two complementary stories. In England, the same legal machinery that protected aristocratic estates from being broken up forced their urban development to be parcel-by-parcel. In France, the same legal machinery that broke up aristocratic estates put the state in charge of urban planning at a much larger scale. The aristocracy was the unit of urban development in England; the state was the unit in France. The size of the development parcel follows directly from which actor’s hands held the pencil.

The urban development mechanism for a London estate ran in five steps, and the geometry is worth tracing precisely. First, an Estate Act of Parliament unfroze the entail for a specific tract - the parliamentary safety valve we discussed. Then the estate office laid out a street grid and subdivided the tract into building plots. The estate signed building agreements with master builders to take substantial blocks of land and develop them under the estate's overall plan; the builders in turn sub-let plots to smaller speculative builders, sometimes also supplying capital and materials. James Burton, for example, erected over 900 houses on the Bedford and Foundling Hospital estates in the decade ending in 1803 on this model. Each house, when finished, was granted a 99-year building lease; the master builder then occupied it, sold the unexpired lease to a purchaser, or let it on shorter subleases. The streets, sewers and pavements were laid by the estate office; the plots filled in plot by plot, never as a single contiguous structure.26

The case of Bedford Square

Bedford Square (1775-1780, designed by Thomas Leverton and built principally by William Scott and Robert Crews under building agreements with the Bedford Estate trustees) is the canonical worked example. The square is roughly 158 by 97 metres between the houses, enclosing an oval communal garden of about 114 by 78 metres. All four sides are built up: 54 uniform four-storey terrace houses with stucco-pedimented centerpieces on each elevation, plot frontages of roughly 22 to 30 feet, every house fronting onto the estate-owned garden. The total footprint of the whole rectangle is about 1.5 hectares - well into the scale at which Continental cities were building perimeter-block apartment buildings around courtyard atriums, yet it produced 54 row houses instead. The reason for that is the next question.

Why no apartment-block developer ever emerged in England

Granted that strict settlement prevented the aristocrat from selling the freehold, and granted that the 99-year cap forced him to lease rather than sell, the leasehold could in principle have been a single big lease over a hundred acres to one large developer who would have built an apartment block. He had the freehold, the trust permitted a 99-year lease: nothing in the legal architecture of strict settlement required that the lease be granted to fifty separate small builders rather than to one large one. So why was it never granted to one large developer?

A set of interlocking constraints answers the question, and once they interact, the small-plot leasehold becomes the only equilibrium the British institutional landscape could support.

Counterparty risk under strict settlement. The estate’s freehold sat in a multi-generational trust whose duty was to provide steady, predictable income for the life tenant, the widow’s jointure, the younger sons’ annuities, and the contingent remaindermen across decades. A single big developer would concentrate the entire revenue stream on one counterparty for the duration of the lease. If the developer failed, the estate’s income failed with him. Spreading the lease across fifty master tradesmen building five houses each diversifies the risk down to the household level. The Bedford and Grosvenor offices both used the small-lessee pattern that is documented across the Survey of London volumes on those estates; the fiduciary logic that produced the pattern follows from the legal structure of strict settlement itself.

The absence of a credit instrument for apartment-block construction in Britain. A row house in the British speculative regime was a short-cycle product. Statistics on Camberwell show that at the 1878-1880 peak, more than half of the borough’s builders completed six or fewer houses in a year and turned their capital over inside it.27 A multi-storey apartment block was a longer and more capital-intensive proposition: construction-cost outlays, ground-rent payments, contractors’ bills and the timing risk of vacancies at completion were spread over several years. In France that risk was absorbed by the Crédit Foncier, which discounted bons de délégation issued by the City of Paris to Haussmann's contractors - the bank held 398 million francs of City-of-Paris paper by 1868.28 In Germany it was absorbed by the Pfandbrief market: the Frankfurter Hypothekenbank of 1862 was the first of about 40 private mortgage banks that, by the beginning of the twentieth century, were concentrated almost entirely on real estate financing in rapidly industrialising cities, lending against apartment buildings’ continuously flowing rent payments - the canonical example of that collateral being the four- to five-storey rental blocks of the Berlin Wilhelmine Ring. In Britain no equivalent instrument for apartment-block-scale construction emerged, and the reason was institutional.

The Bank of England, chartered in 1694 to fund William III’s war against France, grew up as the financial arm of the Whig public-credit coalition that emerged after the Glorious Revolution. Its early directors were drawn predominantly from the Whig party and its capital was lent almost entirely to the state; private business - including early forays into mortgages that appear briefly in the Bank’s eighteenth-century minute books - was a sideline that “soon fell away”.29 Its rivals were Tory-leaning land-bank schemes of the 1690s and, briefly and disastrously, the Tory-led South Sea Company of 1719-1720. The Bank’s operating culture was set by these origins. It made its money discounting short-term commercial paper - bills of exchange drawn on actual goods in transit, to be repaid out of the proceeds of the sale, within weeks or a few months. This was reinforced and codified by the Bank Charter Act of 1844 and the broader “real bills” doctrine that governed nineteenth-century English central banking. Multi-year mortgage credit on urban property was simply not what the Bank’s discount window was designed for.30 France’s Crédit Foncier of 1852, by contrast, was deliberately built around long-duration property credit. It was a state-supervised mortgage bank that issued bonds - the obligations foncières - against a ring-fenced pool of urban-property loans, sold the bonds to French rentiers, and used the proceeds to fund Haussmannian construction under the Second Empire. The two institutions emerged from opposite political economies, and their attitude toward urban real-estate finance followed.

The country banks lent on short maturities. Their funding base was local deposits - withdrawable on demand - and their reserves were thin. Most of their lending was the discount of bills of exchange, the dominant instrument of British short-term credit through the Industrial Revolution. Lending against a construction asset whose first cash flow would arrive only after years of building - and whose underlying collateral, the unfinished building, was illiquid until completion - was not what country banks did, and not what their depositors would have tolerated. A developer who wanted to operate at apartment-block scale in 1860s Britain would have had to fund the multi-year construction window from his own balance sheet. The largest British builders did exactly that, at the terrace-house scale: James Burton erected over 900 houses on the Bedford and Foundling Hospital estates in the decade ending in 1803, and Thomas Cubitt undertook the “almost single-handed creation of Belgravia and Pimlico” from 1824 onward, on Crown- and Westminster-leased land. Their working capital was partnership equity recycled through ground-rent collections rather than long-duration debt secured against future rental flow; the British credit system did not offer the latter instrument.31

A clarification is worth making before moving on. The Continental side did not lack small builders. Berlin, Paris and Madrid had the same long tail of jobbing masons, plasterers, carpenters and joiners that London did; individual building sites in the Wilhelmine Ring or on Haussmann's boulevards were built by many small specialist trades, exactly as in Camberwell or Bloomsbury. What differs across the two systems is not the distribution of construction-firm sizes but the unit that capital flowed to. In Berlin or Paris the financed unit was the apartment block: a Pfandbrief mortgage bank or the Crédit Foncier lent against the building, a Baumeister or a development company assembled the trades, and the small contractors worked beneath that umbrella. In Britain the financed unit was the row-house cluster: a country bank lent against improved ground rents on three to six terrace plots, and the small master tradesman of those plots was the principal developer in his own right. The same trades existed on both sides of the Channel. The institutional unit they aggregated into - apartment block on one side, row-house cluster on the other - was set by the credit architecture, and that unit, in turn, set the built form.

The exit problem. Once an apartment block was built, the developer had two ways out. He could keep it on his own books as a rental-yielding asset, becoming a rentier-corporation in the Continental sense - or he could sell off individual units to occupier-households. Both exits were closed in Britain.

Becoming a rentier-corporation in Britain would have required either a Pfandbrief-like refinancing mechanism, which never developed, or a class of bourgeois savers willing to hold equity in a company against its recurring apartment-rental yield. However, the British saver of 1900 faced an unusually broad and liquid global menu. The British exchange system listed thousands of quoted securities across London and the provincial exchanges; the official London Stock Exchange list itself ran to several hundred domestic companies, with the Stock Exchange Official Intelligence tracking thousands more issues, including a large share of foreign government and colonial bonds. Foreign sovereign and colonial debt traded at meaningful yield spreads over Consols - a reasonable central tendency for the period is 4 to 6% on foreign sovereigns and Indian railway debentures, compared with 2.75% on Consols themselves and the 3.5 to 4% yields then available on top-grade German Pfandbrief paper.32 Consols traded continuously, with dividends paid net of tax through the Bank of England, in practice an administratively light asset for the British holder. A domestic apartment-rental company would have had to compete against this menu on yield, liquidity and perceived political safety. The French saver had a narrower domestic menu - the official Paris Parquet listed around 815 securities in 1900, plus another 396 on the unofficial Coulisse - but he was not captive. Russian sovereign bonds in particular were the first-choice foreign allocation for French savers, accounting for roughly a quarter of French foreign investment by 1914.33 The Crédit Foncier enjoyed a privileged, state-anchored, retail-friendly funding channel for its obligations foncières, rather than a captive demand pool. The directionally right comparison is therefore that London’s saver had a broader and more liquid global menu, which made the domestic apartment-rental company a poor fit on every saver-side dimension; Paris’s saver was also globally exposed, but more easily channelled into state-linked rentes, railway paper and Crédit Foncier bonds.

Joint-stock company formation in Britain has its own story. Recent economic-history work has shown that the 1720 Bubble Act, often invoked as a constraint on joint-stock formation, was in practice “practically a dead letter” - only one prosecution in the entire eighteenth century, and the Act was repealed in 1825.34 The point is therefore not that British company formation was legally blocked. It’s that the British capital that would have funded apartment-block companies in 1855 had already been committed to railway construction in the 1830s and 1840s and to colonial and foreign government issuance in the 1840s-1880s. The Continental joint-stock urban-property company emerged in parallel with the railway era; in Britain the railway era came first, absorbed the available joint-stock capital, and the urban-property-company era never followed. The City of London Real Property Company, founded 1864, is a partial counter-example - but it concentrated on commercial property in the City, not residential apartments, and at a scale an order of magnitude below the Compagnie Foncière. The British bourgeois rentier did not lack appetite for urban-property paper out of culture or temperament. The alternatives on offer were simply better assets on every dimension that mattered to him: yield, liquidity, tax treatment, and administrative simplicity.

Selling off individual apartments was foreclosed by a separate gap. English law did not recognise divisible-by-floor freehold or leasehold ownership before well into the twentieth century. There was no legal instrument by which a developer could sell apartment number 3 of building number 7 to a household buyer. Flying freeholds existed in narrow exotic cases and were not bankable. The Land Registration Act 1925 and the Commonhold and Leasehold Reform Act 2002 are the late legal interventions that finally created that instrument.

The institutional landscape was already taken up. By the 1820s, when the great Bedford and Grosvenor releases were unfolding, the master-tradesman regime was in place across London. Estate offices had decades of experience contracting with master tradesmen; surveyors knew how to lay out small-plot grids; solicitors specialised in 99-year leases and improved-ground-rent capitalisation; country banks knew how to lend against these structures. Any apartment-block-scale entrant in 1875 would have found no available estate land (it was all under existing 99-year leases), no available credit channel, no construction firm at scale, no available exit, and a labour market unfit to support him. The path-dependence is concrete and dated: a developer with the right idea in 1875 could not assemble the supporting institutions in time.

Take any one of these constraints on its own and an apartment-block-scale developer might still have emerged in Britain. Take all of them together and the small-plot leasehold-tradesman regime was the only equilibrium the institutional landscape could support. The legal machinery that protected the great estates’ freeholds across three centuries was the same machinery that forced their urban development to come out plot by plot for those same centuries - not as a circular outcome of “the existing regime”, but as the precipitate of concrete institutional features, the absence of any one of which would have changed the outcome.

Vienna before 1848: apartments without modern finance

To add to the complexity, it turns out the Continental story has a deeper origin than the Code Civil. Vienna had apartment morphology two centuries before bond markets reached it. The Habsburg state’s Hofquartierwesen - the imperial-court billeting system administered from the Hofquartiersamt since the sixteenth century - obliged the owners of taxable “bürgerliche” houses inside the walled city to set aside rooms for the court’s quarter-entitled retinue, while properties belonging to nobility, clergy, the university and other public institutions were exempt as “Freihäuser.” The structural significance is in the share of the housing stock the system touched: Starhemberg’s 1637 survey found that of the city’s roughly 1,210 inner-city houses, 477 acknowledged the Quartier-obligation while 733 claimed Quartier-freedom; by ~1700, 550 inner-city houses were paying taxes to the city.35 About 40% of the housing stock therefore bore a permanent billeting obligation that impaired its use-value and resale price, while the other 60% enjoyed an exemption relieving such pressures.

The market response was systematic: nobles acquired bürgerliche houses and rolled them into Palais precisely to extract the quarter-freedom grant, in what the City repeatedly protested as “the incorporation of townsmen’s houses into noble palaces,” and what the crown itself eventually conceded was “pricing city real estate out of the reach of most ordinary citizens, who now had increasingly to look to the suburbs for housing they could afford.”36 Crucially, the building type that was being incorporated and scaled up was already a vertically stacked, multi-tenant block. The standard substantial Viennese house even before 1700 had ground-floor shops, stables and artisans’ workshops; the owner’s principal floor above; and an upper storey of “small rental apartments” off which “many owners of such buildings, particularly widows, made their living entirely from rentals.”37

The Palais was the same form built grander: a larger courtyard, more storeys, a noble family on the piano nobile, and the same upper-floor rental apartments above. When ordinary citizens were pushed into the Vorstädte - the suburbs, the same morphology - multi-storey courtyard block, mixed use, rented apartment by apartment - was rebuilt at smaller unit size and multiplied across suburban land held by lay corporations, parish foundations, monastic orders (Mariahilf, St. Ulrich, Schottenfeld) and aristocratic investment vehicles such as “the Liechtensteins’ extensive and enormously profitable residential development in the Alsergrund.”38 The Vorstadt Mietshaus was, in other words, the Palais scaled down and repeated. The bond-rentier channel of the Allgemeine Österreichische Boden-Credit-Anstalt arrived only in 1863, and layered modern capital onto an apartment morphology that the Hofquartier exemption had already produced.

This case looks at first like a counter-example to our framework: the Vorstadt was fragmented among many landlords, yet produced apartment buildings. But this is the fragmented ownership thesis we discussed - the case where the scale of the actor at any single parcel diverges from the scale of the city's overall ownership. Both Vienna and Brooklyn were fragmented at the city level. The decisive difference is at the parcel: each Viennese Vorstadt landlord - the Liechtensteins in the Alsergrund, a monastic foundation around its Vorstadt-village holding, a parish corporation on its church lands - controlled a contiguous tract as a single integrated development unit, owning the land, commissioning the building, and managing the resulting rental flow under one roof, whereas in Brooklyn the land passed through chains of speculative subdivision - original estate seller, then speculator, then developer, then small-group row-house builder - so the unit that finally got built was a 20-foot-frontage row house in a group of two to four, not a multi-storey courtyard apartment block. The developer-scale variable in the form equation reads on the parcel-scale actor, not on aggregate city-level ownership. Vienna pre-1848 was an apartment city for the same structural reason that Berlin became one later in the 19th century: large parcels in the hands of single agents, even when the agents themselves were dispersed across the city. Part 3 plugs the rest of the variables into Vienna alongside the other hybrid cases.

Madrid after the desamortización

Madrid arrives at the same morphology as Paris, Berlin and Vienna by a fourth path. Not revolution. Not state-planned extension into farmland by an absolutist state. Not a centuries-old institutional exemption channelling building to the suburbs. Madrid’s path was liberal expropriation - the dismantling of church and feudal-entail estates by successive Spanish liberal governments through statute, with the released land sold to bourgeois proprietors at auction. The desamortización of 1836-1855 (literally “demortmaining”: breaking up estates that had been held in manos muertas, dead hands, by religious orders and feudal entails that could not legally sell) ran under Mendizábal in 1836, Espartero in 1841, and Madoz in 1855. A sequence of statutes placed the lands of religious orders and feudal entails on the open market, and the dissolution created a class of small-to-medium bourgeois proprietors with Roman-law freehold title and liquid savings, facing a city about to expand outward. Carlos María de Castro’s 1860 Plan laid out the Madrid ensanche (literally, “widening” - the formal urban-extension plan; the same concept as the Parisian Haussmann boulevards or the Berlin Hobrecht plan) on large rectangular blocks of about 100 by 100 metres, with perimeter alignment required by the ensanche code.39 The new Banco Hipotecario de España of 1872 - a state-supervised mortgage bank modelled directly on the French Crédit Foncier - supplied the long-duration bond-side credit. The bourgeois proprietors used family-owned immeubles de rapport (multi-storey apartment buildings held by a family or company for the rental income) as their inheritance vehicles. Spanish civil law resembled the Napoleonic réserve in principle through the legítima (the equivalent forced-partition share for the children), so the same partition logic operated; the Banco Hipotecario provided the financing channel the Crédit Foncière provided in Paris.40 The substrate, the block geometry, and the financing channel all pointed the same way, and Madrid became an apartment city built on the same machine as Paris and Berlin, even though the path to that machine ran through neither aristocracy nor revolution.

Huddersfield as the within-Britain control

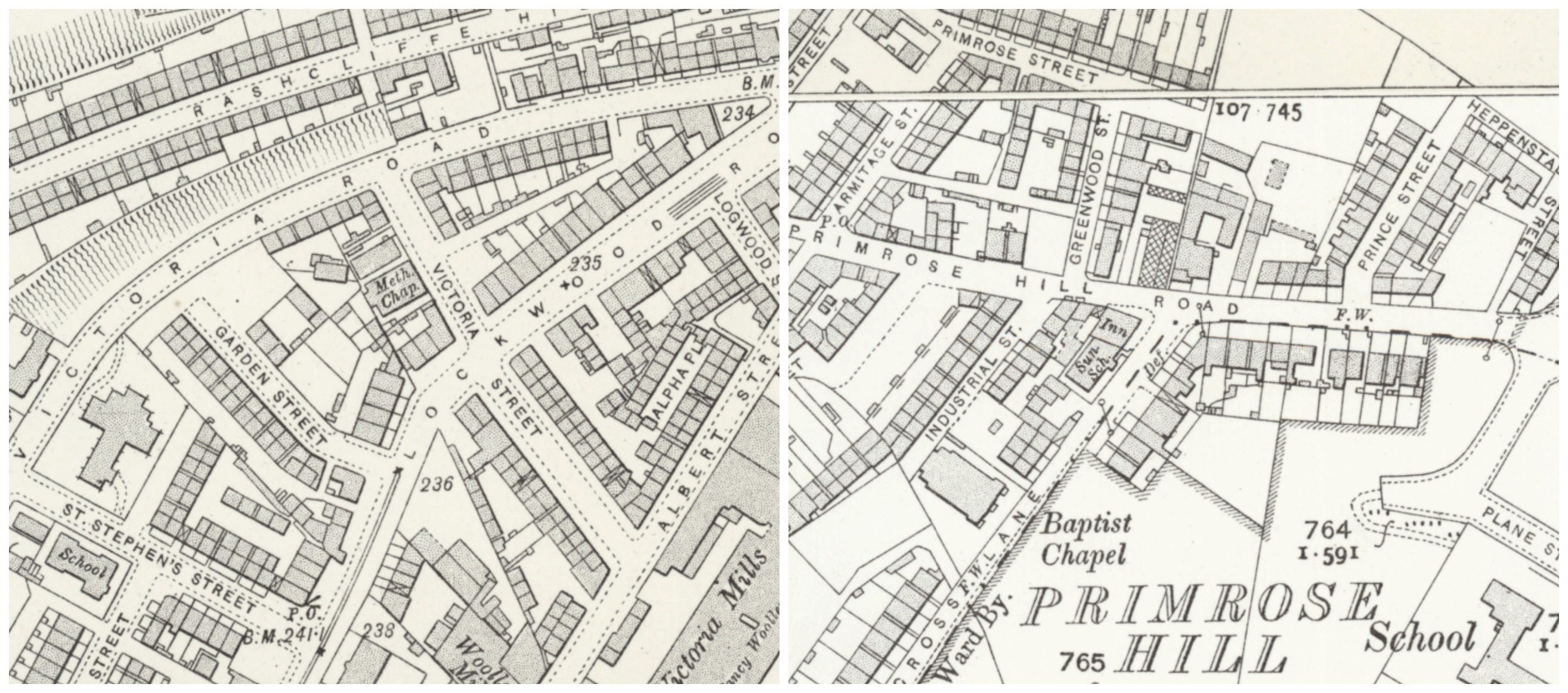

Huddersfield supplies a useful within-Britain control on what a tenure regime can and cannot do. The Ramsden estate held a near-monopoly on the land around the town centre and operated under several leasing arrangements during the 19th century, including the 999-year leasehold that was the regional default in West Yorkshire. The 999-year lease is the interesting test point because it offers, in effect, near-perpetual tenure security - the very condition a developer financing a multi-storey rental investment would want. If long-duration tenure alone could lift Britain into apartment-block construction, this is where it would show up. It does not. Through every shift in the Ramsden estate’s tenure form, the housing that came off the land remained the row house.

The estate also yields a covenant test. At Primrose Hill on Whitehead Lane, the Ramsden boundary met the Lockwood Proprietors’ land along the same stretch of road. Between 1861 and 1865, the Lockwood Proprietors permitted back-to-back houses, and 76 of them were built at an average of 65 square yards per house. The Ramsden estate prohibited back-to-backs by covenant, and the same stretch of road yielded only six through houses at an average of 253 square yards per house - a four-fold difference in density driven by covenant, not by tenure.41 Both sides are still the same building type: a row house, compressed or spaced according to what the covenant allowed.

The conceptual point this experiment controls for is what no single variable inside the English bundle can do. Vary the tenure form alone, and the row house remains. Vary the covenant alone, and the row house compresses or spaces out but remains. The Continental apartment block requires the whole institutional bundle in alignment - forced-partition inheritance pushing capital into rentier corporations, Pfandbrief credit funding multi-year construction against future rental flow, alternatively divisible-by-floor ownership law for the exit, and the rentier-corporation or owner-occupier-mortgage market to absorb completed buildings. Britain had none of those. Huddersfield shows that varying the English variables one at a time inside that incomplete bundle - even the most apartment-friendly tenure available - does not produce apartments.

Wrapping up Part 1

Part 1 has so far set up the substrate and walked one variable up. Part 2 will carry the framework through Berlin’s particular history - from Frederick II’s military finance to the Mietskasernen of the 1890s - and turn to the builder-side and buyer-side credit channels: the mechanism by which a Pfandbrief bondholder in Hamburg priced a Berlin apartment block from standardised tables, and the mechanism by which a small London builder borrowed against future rack rents from a country solicitor, are the two credit channels that put up most of the world’s apartment and row-house stock between 1850 and 1914. In modified form they are still building both today.

Timothy Blackwell and Sebastian Kohl, “Urban heritages: how history and housing finance matter to housing form and homeownership rates”, Urban Studies 56(15) (2018).

Lucas Poy, “A tale of two cities: the tenants’ strikes of 1907–1908 in Buenos Aires and New York” (2021).

William C. Baer, “Landlords and tenants in London, 1550–1700”, Urban History (2011).

David Englander, Landlord and Tenant in Urban Britain, 1838–1918 (Oxford: Oxford University Press, 1983).

Brian Potter, “The Rise of Build-to-Rent Housing”, Construction Physics (May 2026), drawing on National Association of Homebuilders data. Firm-level holding statistics derived from Invitation Homes, American Homes 4 Rent and Tricon disclosures.

Martin Nadaud, speech to the Chamber of Deputies, 1882, calling for the demolition of the Thiers Wall - “la grande ville étouffe dans sa camisole de force” (”the great city is choking in her straitjacket”). Cited in Yves Michaud (ed.), Paris: Université de Tous les Savoirs (Paris: Odile Jacob, 2004), pp. 105–106.

Yair Mintzker, The Defortification of the German City, 1689–1866 (Cambridge: Cambridge University Press, 2012). Mintzker documents that by 1816 about 60 per cent of German cities had already pulled down their walls, and that defortification overwhelmingly preceded industrialisation rather than following from it.

Yonah Freemark, Anne Bliss and Lawrence J. Vale, “Housing Haussmann’s Paris: the politics and legacy of Second Empire redevelopment”, Planning Perspectives (2021).

Richard Rodger, Housing in Urban Britain, 1780–1914 (Cambridge: Cambridge University Press, 1989).

Spiro Kostof, The City Shaped: Urban Patterns and Meanings Through History (London: Thames and Hudson, 1991).

Sonia A. Hirt, Zoned in the USA: The Origins and Implications of American Land-Use Regulation (Ithaca: Cornell University Press, 2014).

Blackwell and Kohl 2018, op. cit. The deposit-based vs bond-based mortgage-institution typology is developed in their Section III.

Francis G. Castles, “The really big trade-off: home ownership and the welfare state in the new world and the old”, Acta Politica 33 (1998); reformulation in Acta Politica (2005).

Antonio Padoa-Schioppa, A History of Law in Europe: From the Early Middle Ages to the Twentieth Century (Cambridge University Press, 2017).

Rafe Blaufarb, The Great Demarcation: The French Revolution and the Invention of Modern Property (New York: Oxford University Press, 2016); French edition, L’invention de la propriété privée: une autre histoire de la Révolution (Seyssel: Champ Vallon, 2019).

Dan Bogart and Gary Richardson, “Estate Acts, 1600 to 1830: A New Source for British History”, working paper (2008), published in Research in Economic History 27 (2010). On the operating logic of strict settlement and the 99-year leasing cap, see also Martin Davey, "Long Residential Leases: Past and Present", in Susan Bright (ed.), Landlord and Tenant Law: Past, Present and Future (Oxford and Portland, OR: Hart Publishing, 2006), 147–170, esp. 150-152, which derives the 99-year cap from the leasing powers of the tenant for life under strict settlement, citing W. S. Holdsworth, An Historical Introduction to the Land Law (Oxford: Clarendon Press, 1927), 233–234.

Andro Linklater, Owning the Earth: The Transforming History of Land Ownership (London: Bloomsbury, 2013). The two-track regime of dynastic-aristocratic land and free-circulating bourgeois capital is treated through the chapters on the Tudor land settlement and on the City of London merchant class.

Ibid.

Ibid.

Kirsten Wandschneider, "Landschaften as Credit Purveyors - The Example of East Prussia" (working paper, October 2012). The Prussian Landschaften emerged after the Seven Years' War as cooperative mortgage associations issuing covered Pfandbriefe against landed-estate collateral. Founded as noble-only cooperatives, they were opened to non-noble estate owners in the early nineteenth-century reforms; by 1834, roughly two-thirds of East Prussian estate borrowers were non-noble. The eligibility test was estate ownership, not entail status - the institutional point Part 1 pursues is the existence of a standardised, bond-issuing mortgage layer secured by real estate, not a specific channel from secularisation to credit.

For the founding: Sidney Homer and Richard Sylla, A History of Interest Rates, 4th edn (Hoboken, NJ: Wiley, 2005), 462, describing the establishment of “a land bank, the Crédit Foncier, in 1852” as one of the Second Empire's measures “to improve the availability of credit to smaller entrepreneurs.” For the financing of Haussmann's Paris specifically: David H. Pinkney, “Money and Politics in the Rebuilding of Paris, 1860–1870,” Journal of Economic History 17, no. 1 (March 1957), which records the Crédit Foncier holding 398 million francs of City of Paris bonds (taken directly or by re-discount) by 1868.

J. A. Lacomba and G. Ruiz, Una historia del Banco Hipotecario de España (1872–1986) (Madrid: Alianza Editorial / Banco Hipotecario, 1990).

Richard Rodger, Housing in Urban Britain 1780–1914: Class, Capitalism and Construction, Studies in Economic and Social History.

Theresa Finley, Raphaël Franck and Noel D. Johnson, “The Effects of Land Redistribution: Evidence from the French Revolution” (working paper, June 2018)

Martin Davey, “Long Residential Leases: Past and Present”, in Susan Bright (ed.), Landlord and Tenant Law: Past, Present and Future (Oxford and Portland, OR: Hart Publishing, 2006), drawing on W. S. Holdsworth, An Historical Introduction to the Land Law (Oxford: Clarendon Press, 1927). Davey, paraphrasing Holdsworth: “the 19th century Settled Land Acts simply codified conveyancing practice.” The 99-year cap on a tenant-for-life's leasing power without a Private Act of Parliament was conventional from at least the 1730s in Bath and 1775 at Bedford Square; the Settled Estates Act 1856 placed it on statutory footing, and the Settled Land Act 1882 (the principal Settled Land Act, sponsored by Lord Cairns) consolidated it.

H. J. Dyos, "The Speculative Builders and Developers of Victorian London," Victorian Studies 11, Supplement (1968).

H. J. Dyos, “The Speculative Builders and Developers of Victorian London,” Victorian Studies 11.

David H. Pinkney, "Money and Politics in the Rebuilding of Paris, 1860–1870," Journal of Economic History 17, no. 1 (March 1957).

Anne L. Murphy, Virtuous Bankers: A Day in the Life of the Eighteenth-Century Bank of England (Princeton: Princeton University Press, 2023). Murphy: “the Bank never seriously pursued private business opportunities. Early in its history there had been some forays into private loans both through ‘pawnes’… and through mortgages. This business soon fell away.” On the Whig-Tory financial rivalry and the Land Bank scheme, see Murphy’s Introduction.

Joel Mokyr, The Enlightened Economy: An Economic History of Britain 1700–1850 (New Haven: Yale University Press, 2009). Mokyr documents the Whig political profile of the Bank's early directors, the South Sea Bubble of 1720 as a Tory-led rival institution, the Bank Charter Act of 1844 (written mostly by Samuel Jones-Loyd, later Lord Overstone), and the dominance of bill-discounting as the operational core of British banking through the Industrial Revolution.

H. J. Dyos, “The Speculative Builders and Developers of Victorian London,” Victorian Studies 11. Joel Mokyr, The Enlightened Economy (New Haven: Yale University Press, 2009), ch. 11, on country-bank deposit funding, partnership constraints, and bill-discounting as the operational core of British banking. The Cubitt biography is Hermione Hobhouse, Thomas Cubitt: Master Builder (London: Macmillan, 1971).

Sidney Homer and Richard Sylla, A History of Interest Rates (Wiley, 4th edn 2005), comparing British Consols with Prussian and Imperial German bonds: “German bond yields, however, were almost always substantially higher than yields on British consols; after 1845 there was a tendency for the differential to widen.” The 4-6% / 3.5-4% figures are a central tendency for late-nineteenth-century foreign sovereign / Pfandbrief paper from this series; specific years and instruments show variation.

For the size of the Paris market in 1900 (Parquet vs Coulisse) and the share of Russian and other foreign sovereign bonds in French portfolios, see Pierre-Cyrille Hautcoeur and Angelo Riva, “The Paris financial market in the nineteenth century: complementarities and competition in microstructures”, Economic History Review (2012), supplemented by the standard literature on French savers and Russian sovereign debt before 1914.

Mokyr.

Josef Kallbrunner, Wien im 17. Jahrhundert: “von den zirka 1210 Häusern der inneren Stadt nur 477 die Quartierpflicht für sich anerkannten, während 733 quartierfrei zu sein behaupteten.” John P. Spielman, The City and the Crown: Vienna and the Imperial Court, 1600-1740 (West Lafayette, IN: Purdue University Press, 1993): “there had probably never been more than 1,250 houses in the inner city and fewer than that in the suburbs,” with the city counting “only 550 within the walls and 450 outside” paying taxes by ~1700.

John P. Spielman, The City and the Crown: Vienna and the Imperial Court, 1600–1740 (West Lafayette, IN: Purdue University Press, 1993).

Spielman, The City and the Crown, on the standard substantial Viennese house c. 1700: “richer families generally had much larger houses with a courtyard and a second story of living quarters, part of which would have been designed specifically as small rental apartments. Many owners of such buildings, particularly widows, made their living entirely from rentals.”

Spielman, The City and the Crown: “The old suburbs had mostly been clusters of small houses built closely together on land protected by some special jurisdiction of lay corporations (Spittelberg, Windmühl, Auf der Wieden, Rossau, etc.) of parishes or monasteries (Mariahilf, St. Ulrich, Schottenfeld) or of an aristocratic investment such as the Liechtensteins’ extensive and enormously profitable residential development in the Alsergrund.”

Costa Frank J. Dr., Noble Allen G. Dr. & Pendeleton Glenna, “Evolving planning systems in Madrid, Rome, and Athens,” GeoJournal. 24 (3): 294 (1991).

For the Banco Hipotecario de España: founded by law of 2 December 1872 with the original concession granted to Banco de París y de los Países Bajos (Paribas) (the French connection is direct) formally constituted 15 April 1873, granted the unique privilege to issue cédulas hipotecarias in 1875, with the Spanish state participating in the bank's profits while it held the privilege. See J. A. Lacomba and G. Ruiz, Una historia del Banco Hipotecario de España (1872–1986) (1990); see also Manuel Valverde Villa, El Banco Hipotecario de España: Historia de sus operaciones hipotecarias (2023), and the comparative placement in Timothy Blackwell and Sebastian Kohl, “Urban heritages: How history and housing finance matter to housing form and homeownership rates,” Urban Studies 55. For the Spanish legítima, see Civil Code (Royal Decree of 24 July 1889), Arts. 806-808, and Sergio Cámara Lapuente, “Forced Heirship in Spain,” in Kenneth G. C. Reid, Marius J. de Waal and Reinhard Zimmermann (eds.), Comparative Succession Law, Volume III: Mandatory Family Protection (Oxford: Oxford University Press, 2018). The legítima descends from medieval Castilian and Visigothic law and is older than the Napoleonic Code's réserve héréditaire, but the two systems implement the same forced-partition logic in favour of descendants.

Jane Springett, “Landowners and urban development: the Ramsden estate and nineteenth-century Huddersfield”, Journal of Historical Geography 8(2) (1982).

What a privilege to read. You have made me think about cities in a completely new way - looking forward to the next part!

Fascinating study